Page 218 - Bank Muamalat_AR24

P. 218

216 BANK MUAMALAT MALAYSIA BERHAD

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2024 (29 JAMADIL AKHIR 1446H)

2. MATERIAL ACCOUNTING POLICIES (CONT’D.)

(b) Financial assets (cont’d.)

(iv) Impairment of financial assets (cont’d.)

(1) Determining a significant increase in credit risk since initial recognition (cont’d.)

The assessment of significant deterioration since initial recognition is critical in establishing the point of

switching between the requirement to measure an allowance based on 12-month ECL and one that is

based on lifetime ECL. The quantitative and qualitative assessments are required to estimate the significant

increase in credit risk by comparing the risk of a default occurring on the financial assets as at reporting date

with the risk of default occurring on the financial assets as at the date of initial recognition.

The Group and the Bank assigns each counterparty, financial securities and financial instrument, credit

rating at initial recognition based on available information about the counterparty, financial securities and

financial instrument. Credit risk is deemed to have increase significantly if the credit rating has significantly

deteriorate at the reporting date relative to the credit rating at the date of initial recognition.

Nevertheless, regardless of the change in credit rating, a backstop is applied and a financial asset is

considered to have experienced a significant increase in credit risk if the financial asset is more than 30 days

past due on its contractual payments. In addition, the Group and the Bank may determine that an exposure

has demonstrated a significant increase in credit risk based on certain qualitative factors using its expert

credit judgement and, where possible, relevant historical experience that are considered to be indicative of

such increase whose effect may not otherwise be fully reflected in its quantitative factors.

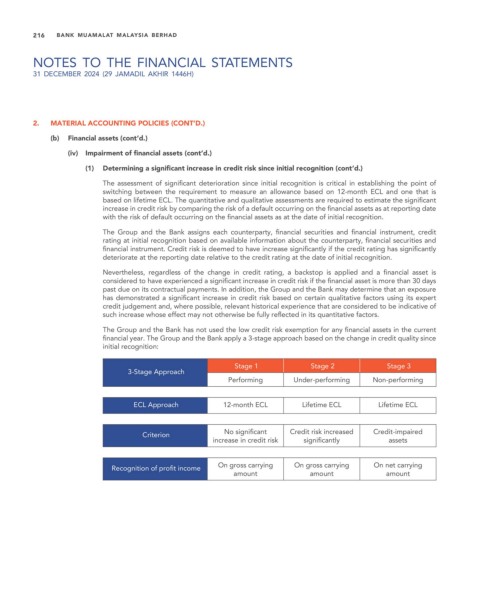

The Group and the Bank has not used the low credit risk exemption for any financial assets in the current

financial year. The Group and the Bank apply a 3-stage approach based on the change in credit quality since

initial recognition:

Stage 1 Stage 2 Stage 3

3-Stage Approach

Performing Under-performing Non-performing

ECL Approach 12-month ECL Lifetime ECL Lifetime ECL

Criterion No significant Credit risk increased Credit-impaired

increase in credit risk significantly assets

Recognition of profit income On gross carrying On gross carrying On net carrying

amount amount amount