Page 370 - Bank Muamalat_AR24

P. 370

368 BANK MUAMALAT MALAYSIA BERHAD

BASEL II

PILLAR 3 DISCLOSURE

3.0 RISK MANAGEMENT (CONT’D)

Risk Governance (cont’d)

Other management-level risk committees are set up to oversee specific risk areas and its related control functions as

described below: (cont’d)

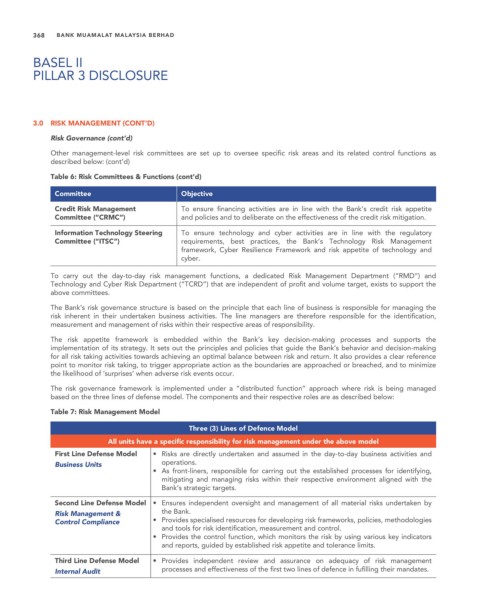

Table 6: Risk Committees & Functions (cont’d)

Committee Objective

Credit Risk Management To ensure financing activities are in line with the Bank’s credit risk appetite

Committee (“CRMC”) and policies and to deliberate on the effectiveness of the credit risk mitigation.

Information Technology Steering To ensure technology and cyber activities are in line with the regulatory

Committee (“ITSC”) requirements, best practices, the Bank’s Technology Risk Management

framework, Cyber Resilience Framework and risk appetite of technology and

cyber.

To carry out the day-to-day risk management functions, a dedicated Risk Management Department (“RMD”) and

Technology and Cyber Risk Department (“TCRD”) that are independent of profit and volume target, exists to support the

above committees.

The Bank’s risk governance structure is based on the principle that each line of business is responsible for managing the

risk inherent in their undertaken business activities. The line managers are therefore responsible for the identification,

measurement and management of risks within their respective areas of responsibility.

The risk appetite framework is embedded within the Bank’s key decision-making processes and supports the

implementation of its strategy. It sets out the principles and policies that guide the Bank’s behavior and decision-making

for all risk taking activities towards achieving an optimal balance between risk and return. It also provides a clear reference

point to monitor risk taking, to trigger appropriate action as the boundaries are approached or breached, and to minimize

the likelihood of ‘surprises’ when adverse risk events occur.

The risk governance framework is implemented under a “distributed function” approach where risk is being managed

based on the three lines of defense model. The components and their respective roles are as described below:

Table 7: Risk Management Model

Three (3) Lines of Defence Model

All units have a specific responsibility for risk management under the above model

First Line Defense Model • Risks are directly undertaken and assumed in the day-to-day business activities and

Business Units operations.

• As front-liners, responsible for carring out the established processes for identifying,

mitigating and managing risks within their respective environment aligned with the

Bank’s strategic targets.

Second Line Defense Model • Ensures independent oversight and management of all material risks undertaken by

Risk Management & the Bank.

Control Compliance • Provides specialised resources for developing risk frameworks, policies, methodologies

and tools for risk identification, measurement and control.

• Provides the control function, which monitors the risk by using various key indicators

and reports, guided by established risk appetite and tolerance limits.

Third Line Defense Model • Provides independent review and assurance on adequacy of risk management

Internal Audit processes and effectiveness of the first two lines of defence in fufilling their mandates.